February 2, 2022 · 12 min read

Emerging Tokens - 2nd February 2022

Liquidity mining is so yesterday - The liquidity wars in DeFi 2.0.

Disclaimer: In the interest of full-disclosure, some members of Novum Insights (not including this article’s author) are currently holders of tokens in collections discussed in this article.

Liquidity mining was the main activator that drew in tens of billions of dollars in the DeFi markets. Through liquidity mining, crypto asset holders were incentivized to supply liquidity to DeFi protocols and be rewarded with new tokens. Airdropped governance tokens skyrocketed in price, eye-opening APYs lured investors in, and in some lending protocols’ cases, users were “paid” with tokens to borrow crypto.

This certainly did boost the TVL in DeFi. What was less than $10 billion prior to the DeFi Summer is now at $81 billion. However, most early liquidity miners yielded high returns, dumped their tokens and their liquidity supply from DeFi protocols as soon as liquidity incentive programmes ended and went off looking for the next liquidity mining opportunities. Many projects then struggled to sustain deep liquidity for their users. It was time to think about better ways for new projects to bootstrap liquidity.

This week at Novum Insights, we look at projects that take different approaches to attracting liquidity. We look at Protocol Owned Liquidity, Liquidity as a Service, and bribing.

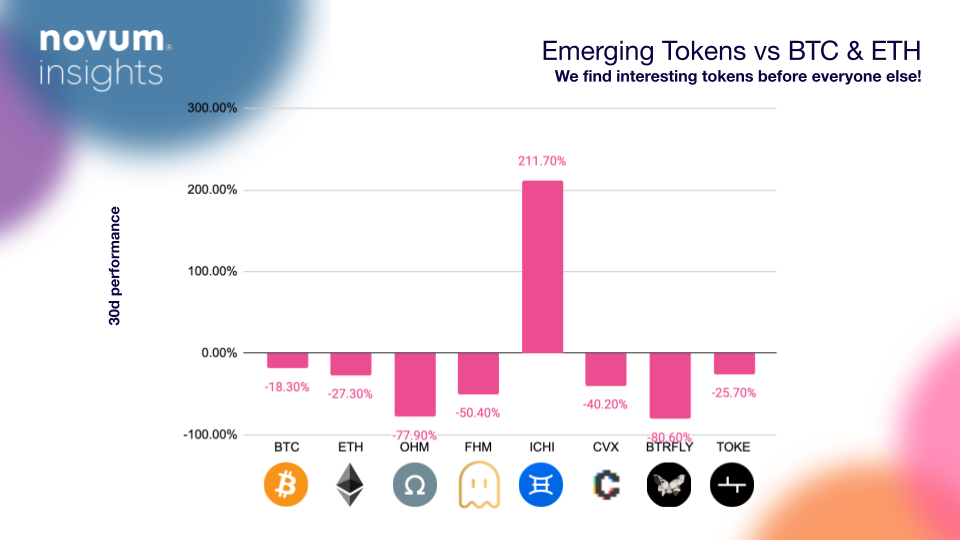

Last Updated: February 2nd 2022 12:30pm GMT

Olympus DAO and its forks FHM and BTRFLY all underperformed BTC and ETH. This shows that rebasing mechanisms can be risky especially in bear markets. TOKE slightly outperformed ETH, and the clear winner of the month of January is ICHI.

Olympus DAO (OHM)

Olympus DAO owns its liquidity through a bonding mechanism. Investors buy OHM at a discount in exchange for their LP tokens. These tokens are then owned by the DAO treasury and accumulate trading fees. If you want to learn about how the discount rates are calculated in detail, see here.

Olympus helps other projects to acquire their own liquidity via the Olympus Pro platform. DeFi protocols that are available on Olympus Pro include Alchemix, Frax, Spaceshift, Blackpool, ICHI, THORswap, KeeperDAO and more. Taking Alchemix for example, the native token ALCX bonds can be purchased at a discount rate. The bonds have a vesting period and will be released steadily over time so that Alchemix prevents the buyers from selling them for a quick profit.

Olympus DAO is a project that aims to become a reserve currency in DeFi. The native token OHM is a free-floating currency backed by a basket of crypto assets. 1 OHM is always backed by 1 DAI, so when OHM trades below 1 DAI, OHM is burnt. When OHM trades above 1 DAI, it means that the expected returns by holding or staking OHM is translated to market premium. OHM is currently trading at $66.31, over 95% lower from its all-time highs. Comparing Olympus’s floor price of 1DAI to its risk-free value (RVF) which signifies the amount of stablecoin funds that is guaranteed to back OHM, it is trading at a 25x premium. The current OHM market cap of $607 million is still higher than the market value of treasury assets ($545 million). When OHM’s market cap reached $4 billion in November 2021, OHM market cap / treasury book value was over 4x.

APYs of hundreds of thousands of percent and the inflationary nature of “rebasing” tokens have caused the investors to question whether OHM was a ponzi. Even though high APYs could possibly offset the rebasing effect and an extreme volatility in price, the price slip of over 90% in less than two months, even after having taken into account the wider downturn of the crypto market, is not negligible. Some argue that the price volatility is not a good metric to monitor regarding the project’s long term vision, but the growth of its treasury should be the metric of importance as OHM is designed to be a DeFi reserve currency, and generates revenue through its treasury holdings.

Due to the complex nature of rebase tokenomics, price volatility, early game theory concepts in DeFi, only users who established a firm belief in DAOs and bonding approach to liquidity should consider investing in Olympus DAO.

Before we move onto the next project, let’s quickly look at one of the most popular Olympus forks, FantOHM (FHM). Built on Fantom with a cross-chain capability with Moonriver, FantOHM mainly distinguishes itself from Olympus DAO via its FHUD stablecoin. FHUD is a FantOHM USD that is created by burning FantOHM’s native token FHM sitting in the DAO account via the proof-of-burn mechanism. So if $10 million worth of FHM token gets burnt, this will mint 10 million FHUD tokens, that is not tradable. These 10 million tokens will be deposited to the treasury. This will unlock 10 million DAI to be transferred to the DAO account to be used in purchasing assets that will generate value. These purchased assets will be then put back into the treasury. This enables an effective use of FHM without affecting its market value and of treasury’s stablecoins while maintaining the Risk Free Value of the treasury.

FantOHM holds $23 million in treasury and FantOHM has a current staking APY of over 290k%! This is a lot higher than OHM’s 1099%. However FantOHM can only sustain this APY for 196 days when Olympus DAO can sustain its APY for 374 days. In the case of book value per governance token, FTM has a higher multiple of 44 compared to OHM’s 25.

ICHI (ICHI)

ICHI is another project that is working on building project-owned liquidity. Ichi takes a stablecoin approach to this. Ichi helps any crypto project or community to mint their branded dollars as USD pegged stablecoins (e.g. Uniswap’s branded dollar is oneUNI) that are redeemable 1 for 1 for USDC. With branded dollars, projects can grow their protocol value by locking away their project tokens to its treasury while users can benefit from stablecoin’s usability in the DeFi space. More than $20 million worth of oneToken has been minted so far and the crypto projects that have deployed ICHI stablecoins (oneTokens) include Uniswap, 1Inch, Fuse, Dodo, Filecoin, Spaceshift FOX and more. If you want to learn more about how to mint branded dollars, read our previous coverage on ICHI here.

ICHI took an extra step into project-owned liquidity with its Angle Vaults. Angle Vaults are a Uniswap V3 liquidity management protocol that enables users to deposit single-sided assets to Uniswap V3. An Angel Vault creates a pool paired with project’s oneToken and the project token (or ICHI). ICHI’s Angel Vault only receives the oneToken from the pool, and uses that to provide buy-side liquidity on the ICHI platform. As the price of the project token (or ICHI) changes, the Angle Vault rebalances. This process makes sure - 1) the users are incentivized to contribute to the long term growth by minting oneToken (locking the project token) 2) LPs earn more Uni V3 fees and thus keep providing liquidity to the project pool.

ICHI is the governance token of the Ichi protocol. ICHI is hard capped at 5 million and more than 4 million ICHI tokens are currently circulating. The current market cap of ICHI stands at $73 million, and ICHI is trading at $17.43, 39% below its ATH back in November, and above 85% since we covered ICHI as one of our emerging tokens a few weeks ago!

Convex Finance (CVX)

Convex Finance is a CRV rewards booster. To understand Convex Finance and the “bribing” phenomenon in DeFi, a quick recap of Curve Wars is necessary. Curve introduced the veCRV (vested CRV) and let the veCRV holders vote on Curve gauge weights. This means that they can redirect CRV emissions towards their desired pools and LPs in those pools can thus receive boosted rewards.

Convex Finance is the most influential platform that is built on top of this trend. Convex Finance distributed more than $400 million since launch in spring 2021 and controls about 40% of circulating CRV. Via Convex, CRV holders can stake CRV. Pooled CRV is then converted to veCRV for boosted rewards. CRV stakers receive a share of boosted rewards, and CRV LP token stakers on Convex are eligible for trading fees and boosted rewards. This can be understood as “bribing” because Convex obtains influence over CRV emissions by helping users earn higher yields.

Convex Finance’s CVX token can also earn a share of boosted CRV rewards via staking. The total supply of CVX is capped at 100 million, and 50% is allocated to pay out CRV LP rewards and 25% is allocated to liquidity mining. 48% of the total supply is currently circulating. Convex charges a 16% performance fee on CRV revenues. CVX is available at major exchanges such as Binance, Gate.io, Sushiswap, Uniswap, Huobi and will be listed on Kucoin today. As the Curve Wars intensified, CVX price more than doubled in December 2021 and hit the ATH of $62.69. CVX is now trading 55% below that.

Convex contributed to the growing ecosystem of Curve, opening the next chapter in DeFi and popularized the “bribing” model. However, much concern is voiced about this trend because gaining monopoly over a project’s governance is the farthest thing from decentralization.

Redacted Cartel (BTRFLY)

Redacted Cartel is a melange of the two widely talked about concepts in DeFi. Olympus DAO’s bonding and Curve bribing. Redacted Cartel is a fork of Olympus DAO that has recently entered the Curve War scene. Redacted Cartel’s native token BTRFLY works like OHM. BTRFLY tokens are a rebase token that can be purchased at a discount in exchange for CRV, CVX or OHM. The deposited assets will be deployed for yield generation.

Apart from those initial assets mentioned above, Redacted Cartel started to pool FXS that employs the vested token model like Curve, and TOKE, liquidity as a Service protocol. Redacted plans to keep absorbing important governance tokens that shape the DeFi ecosystem and influence them.

The project’s BTRFLY token was launched less than two months ago and reached its ATH of $3729 in early January this year. Since then it tanked by 85% along the many other Olympus forks and the general bear market. Redacted Cartel has $79 million in treasury and BTRFLY’s current market cap stands at $164 million, which is more than double the treasury value. The most heavily owned governance token owned by Redacted Cartel is CVX. Redacted Cartel is the fourth biggest DAO in terms of the number of CVX owned. The detailed treasury breakdown can be found here.

Tokemak (TOKE)

Tokemak is a liquidity routing service. LPs of Tokemak provide liquidity via single asset staking, and Liquidity Directors (LDs) control where the liquidity flows. Tokemak’s Token Reactors are where project tokens such as OHM, TCR, VISR, APW, FOX and SNX are deposited, and Pair Reactors receive ETH or stablecoins. Deposited single assets are paired (Token Reactor / Pair Reactor) and deployed as liquidity across various DeFi venues - understood as Liquidity-as-a-Service. There is currently $1.5 billion locked in Tokemak.

LPs earn variable APR rewards in TOKE. LDs are the participants who stake TOKE and make votes to direct certain assets as liquidity to a preferred exchange / protocol. LDs also earn variable APR rewards in TOKE for directing liquidity. The APRs for liquidity directing range between 26% - 43% as of writing. To understand the reward logic better, read this. Tokemak’s impermanent loss mitigation strategies are also outlined here.

As Tokemak’s liquidity pairing approach gained traction, the Toke Wars similar to the Curve Wars ensued. Votemak, a protocol designed to bribe TOKE holders, has been acquired by Redacted Cartel.

TOKE has a total supply of 100 million. 30% of them is allocated as rewards and will be emitted over 2 years. TOKE is trading at $31 and has a market cap of $301 million. The RSI is relatively low at 38, and the RVI started to show a positive trading signal only a few days before. TOKE underperformed BTC and ETH in the past two weeks, but Tokemak designed an interesting liquidity solution. So DeFi participants who want to control where to direct liquidity with Tokemak, this is not a bad moment to buy the dip.

Conclusion

Mercenary liquidity causes DeFi projects headaches. As a solution to this, some protocols started to claim ownership of their liquidity. Protocol Owned Liquidity freed up projects from having to “rent” liquidity from users. Many projects whose core mission is to soak up as much liquidity as possible so as to have a great influence in gauge weights sprung up. However, there is also a risk to this. The accumulation of liquidity by a single entity resembles how the centralized legacy institutions work. The fast innovating DeFi space will soon tell whether the community had been working together to accomplish a common goal or had been handing over the power to few.

Written by Jessica Kang for Novum Insights.

The information provided on this website by Novum Insights is for informational purposes only, we make no warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the website or the information, products, services, or related graphics contained on the website for any purpose. Any reliance you place on such information is therefore strictly at your own risk. None of the information provided is intended nor should be relied upon for the purposes of investment.

The Emerging Tokens Alert and the Novum Blog are based on entirely estimated historical returns which provide no guarantee, promise or calculation of potential future returns or losses. In addition, all of the assets displayed and shown on the website are highly volatile and risky.